USG kills Anthropic Fable 5, and the future of America's software empire

The ecstasy and decline of getting high (margins)

Long time readers will recall that I launched Securities in January 2022 to look at the complex tradeoffs at the intersections of science, technology, finance and the human condition — basically, anything that’s on my mind. Later, I announced the “Lux Riskgaming Initiative” in February 2023 and officially launched Riskgaming in April 2024, merging Securities into that newsletter as one bundle.

Since then, more than 1,000 players have joined our runthroughs in person, we’ve hosted games all throughout the world (most recently Phoenix last week with a brand new game on AI energy systems), and of course, Laurence Pevsner joined us at Lux as my co-partner.

With so much activity now, I decided it made sense to split Riskgaming and Securities once again to allow you to read what you want and skip the rest. Riskgaming will have our new scenarios, posts on game design and event announcements, while Securities will continue as the canvas for my analysis. Lux Recommends, which just hit its 500th edition, has been retired as a separate email to save inbox space, but I’ll append great links I enjoy at the end of these posts.

I always love hearing from readers – please hit reply to reach out!

Breaking Note: Overnight on Friday after I wrote this essay, the U.S. government informed Anthropic that it would ban foreign nationals from using the company’s Fable 5 and Mythos 5 models. The main thesis here stands even stronger given this latest policy action.

With this week’s launch of Claude Fable 5, America’s software industry is crescendoing to an unprecedented climax. Soon the trio of SpaceX (aka xAI), Anthropic and OpenAI will have all gone public, broadcasting their S-1 results and showing to the world what insiders have known for a while: American AI has unearthed a veritable gusher of cash. Their collective growth is faster than the American software industry has ever seen before. In fact, no industry in history has gone from not existing to hundreds of billions of dollars in revenue in roughly four years. Dot-com, railroads, oil, autos — they’ve got nothing on AI.

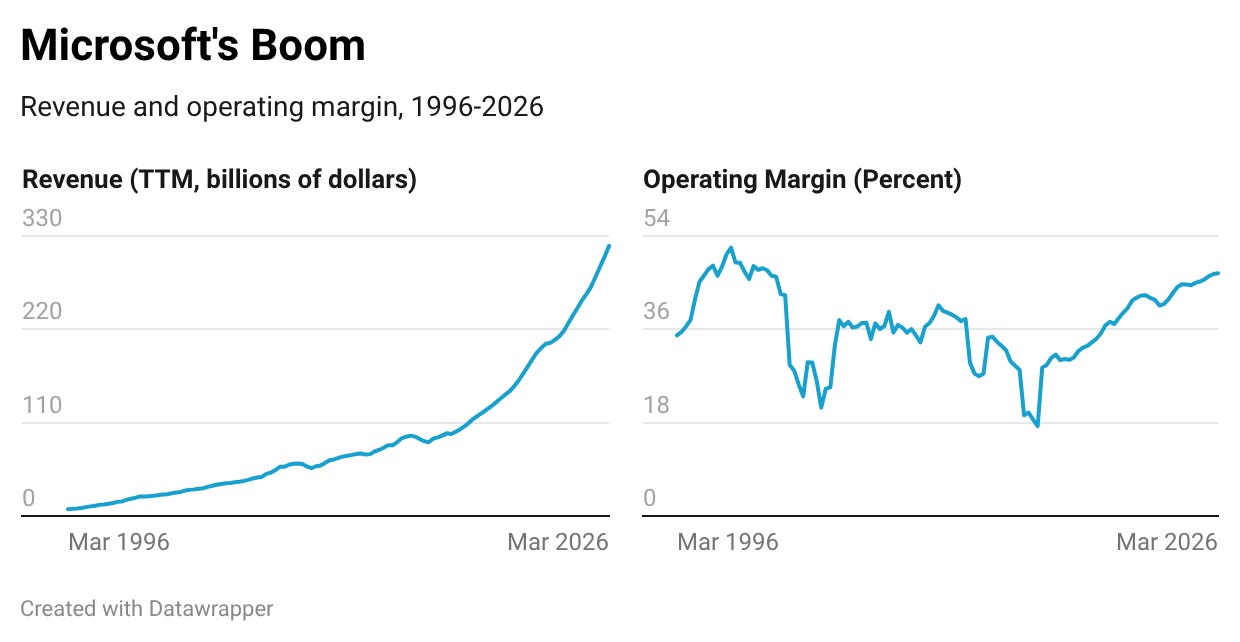

Yet, this trio is just the latest special forces teams of America’s vast software empire. Apple’s iOS hit a record market share the past quarter in the growing but mature smartphone category, with the iPhone 17 becoming the bestselling iPhone of all time. The duopoly of Alphabet and Meta dominate the global internet advertising marketplace, with Google posting a record high operating margin last quarter. Then there’s Microsoft, whose expanding tentacles from cloud infrastructure and developer tools to Xbox consoles have allowed it to grow revenues from $17 billion in 2012 to a record of nearly $83 billion last quarter, all while expanding operating margin to an astonishing 46.8% — the highest in decades. Just take a look at these two charts:

It’s one thing to have an exponential curve in the first decade of a company. It’s something more … imperial to have it be exponential over decades with the occasional blip for recession or war. That’s all while the company has improved its operating margins to levels last seen in the dot-com bubble.

In short, dominant doesn’t even begin to describe America’s software empire. This is not Rome. There are no alternatives globally, no other secret empires across the oceans that might offer even the slightest counterbalance. There’s not even a sign of barbarians outside the gates. No one — certainly not venture capitalists — believes that the leaders of key software verticals have a chance of being displaced in the short-to-medium term.

Yet, the ecstasy of the high is always followed by the depression of the withdrawal. There may not be hordes of barbarians that splash the front pages, but there are indeed bands of rebels that are intensifying their focus on undermining the empire from outside — and within.

First, we have to look at how margins are being threatened by the software industry itself. Fatigue by consumers and enterprises alike, tightening budgets in a K-shaped economy, and historic new competition from coding agents underline potential threats to the software profit gusher.

Second are the threats from home, where a domestic techlash is growing in the form of a strategic reversal on high-talent immigration, a rising chorus against data centers, and a continued elite movement toward antitrust action. America is the brain gain capital of the world, and the most impactful talent still broadly want to come to the land of liberty. Yet, the processes are getting more opaque, more arbitrary.

Then there’s the domestic hatred of AI. The polls are clear: Americans despise AI with more passion than any other country in the world. If the success of America’s software empire has even partially rested on the apathy of American voters toward its most dynamic industry, that equation no longer computes. The rebels aren’t at the gates; in fact, they are already inside. That’s provided the timber to fuel more elite action around tech antitrust, which is mostly in abeyance under the current administration but feels ripe for the 2028 presidential election.

Third and finally, more countries are increasingly militant about removing American software from their infrastructure and instead relying on local and open-source options to buttress their own sovereignty. This pattern can be seen in France, the Netherlands and much of the European Union, but it’s hardly limited there; similar patterns can be seen in the Middle East, India, Brazil, Korea and elsewhere. The increasingly mercurial and arbitrary nature of U.S. software power is breaking long-time purchasing defaults. Add in the rise of compelling if lagging open-source AI models predominantly from China like DeepSeek‘s V4, and there are reasons to expect that last decade’s dominance might be the next decade’s decay.

Empires rarely collapse overnight, but the failures in their underlying logic tend to expand over time and subsume them. Just as American software is hitting its acme from revenues to high margins is when we should be most paranoid that what we’re witnessing are the best days, and twilight might be on its way.

Software was eating the world until an Ozempic plunge

To understand some of the cracks that are forming in the impenetrable wall of software, we have to work our way back to how America’s software empire came to be.

Software has been the lifeblood of venture capital and the broader tech innovation ecosystem since Microsoft and Apple were founded in the mid-1970s. Despite booms and busts across the 1980s and 1990s, software really came into its own in the late 2000s with the quadruple impact of enterprise cloud infrastructure and apps as well as consumer mobile and social.

The vanguards all launched within a short window of each other. Within the span of just one week, Google would launch Google Docs on March 9, 2006, while Amazon unveiled Amazon Web Services on March 14. Together, they reimagined the future of enterprise apps and enterprise infrastructure away from proprietary licenses and hardware mainframes and toward more flexible billing and platform architectures. In September, Facebook would launch its News Feed and also open its social network to all users over 13. Later in July 2008, Apple launched the App Store, transforming the experience of installing software from buying CDs in boxes at Circuit City to over-the-air updates.

These were just a few of the leaders that would completely reformat the entire technical stack of enterprise and consumer computing. From roughly the Great Financial Crisis in 2008 through 2021, American software would expand at a delirious pace, with Marc Andreessen prophetically laying out the trend in his August 2011 op-ed in the Wall Street Journal on “Why Software Is Eating The World.” Ultimately, hundreds of companies reached unicorn status, a term coined in a November 2013 TechCrunch column by Aileen Lee of Cowboy Ventures.

For younger readers, it can be almost impossible to describe how bad software was and how much better it would become in this era. Despite the self-flagellation of Silicon Valley developers and designers about the ephemerality of coding frameworks and UX, the reality is that a tremendous evolution took place. A horrifying spaghetti bowl of kludge code that once ran financial payments for a company could be replaced with a single migration to Stripe. New affordances like mobile forced new abstractions, and with it, serious progress for every user.

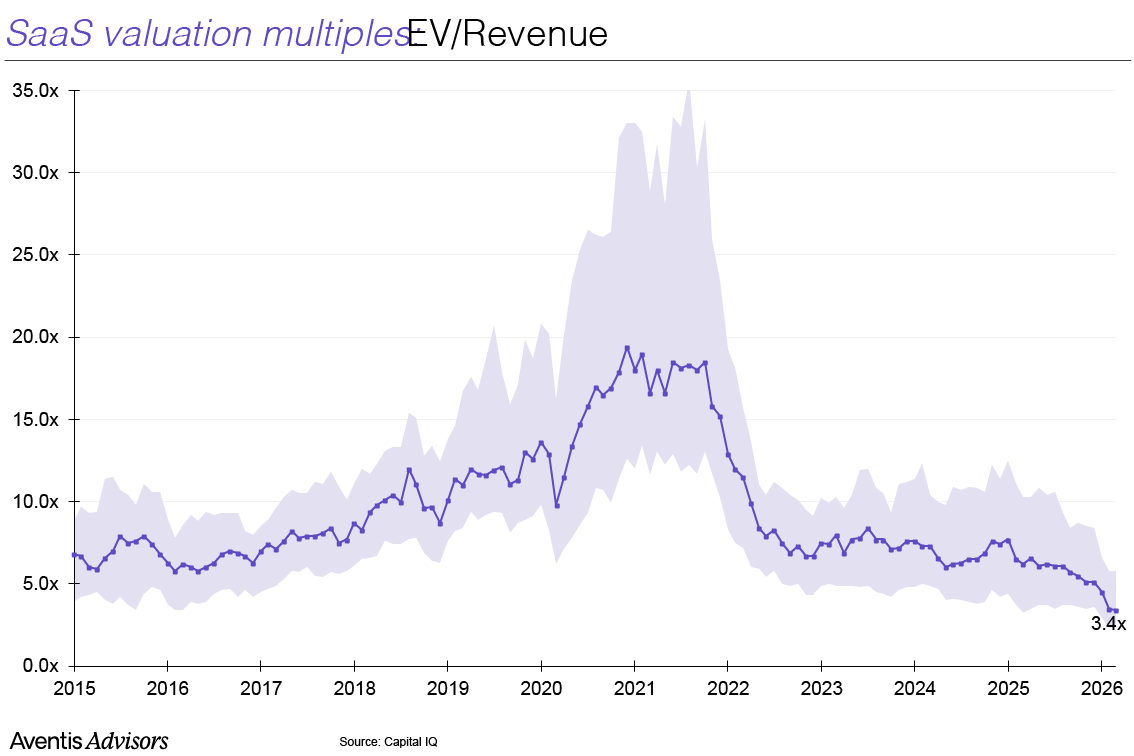

Software grew for about 15 years, and then it crashed, and it crashed hard. Here’s a chart from Aventis Advisors of the software industry’s past decade showing the rise and fall of revenue multiples of software-as-a-service (SaaS) companies:

There are a number of reasons for the reversal that started in late 2021 and 2022, most notably fears that AI models could outright replace software. The less heralded but more important reason though is simply that companies and consumers alike seemed to stop buying new software after the Covid pandemic. According to Okta, enterprises have flatlined on purchasing new software apps for years. That’s not surprising: at an average of 101 apps per enterprise, each employee costs thousands and possibly tens of thousands of dollars in software. Over in consumer, users largely stopped installing new apps on their phones, a trend that was already visible in 2016.

That slower potential growth undermined the core engine of most software businesses, which centered around their crazy-high gross margins. SaaS companies are expected to have 70% gross margins at a minimum, with some of the best companies reaching 85% or better.

It’s really hard to overemphasize how wild that scale of leverage is. For every $1 coming into the business, only about $0.15 is being used to service the customer’s contract (accounting methodologies vary, even after ASC 606). That leaves $0.85 to invest in sales and marketing, software development and other areas for expansion. Companies could go from a kernel of an idea with a six-slide PowerPoint deck to a multi-billion dollar unicorn in just a handful of years through product-led growth and aggressive sales.

The world eventually caught up. After a glut of new software purchases in the remote work years of Covid, CFOs started aggressively auditing usage and seats to cut back on wasteful spend. Meanwhile, consumers started getting subscription fatigue or entered what I dubbed “subscription hell” all the way back in 2018. The friction to installation became higher — and even higher was shelling out real dollars for software.

Venture capital also became insane during Covid, with practically unlimited competition in some lucrative sectors, since software companies often had no moat outside of contract lock-in. Cloud providers started sparring with each other, but the real damage was in enterprise apps. Fear of competition was already palpable by late 2021, but was intensified with the launch of OpenAI’s ChatGPT in November 2022. Fast forward to today where every investor fears that coding agents will simply displace all other software apps. As one investor recently told me, “I wouldn’t want anyone to become a software CEO these days.”

Everyone in Silicon Valley understands that high margins are the key ingredient to venture-scale success. Without them, there is no way to leverage a business for rapid growth. Compare to restaurants: Shake Shack opened its first permanent store in 2004, and today it has about 700 locations and made $1.45 billion in revenue in fiscal year 2025. The difference in growth velocity is margin: Shake Shack needs per-store operational profits to underwrite debt to expand to new locations, which adds a massive time delay to expansion. Software never knew such constraints, which is why Anthropic is adding Shake Shack’s revenue every few days.

Yet constraints for at least some startups came. Investors and startups execs started to emphasize more sustainable growth that took into account the maturing software market. Unfortunately, that undermined the very reason that software was so exciting for investors in the first place, which was its rapid growth compared to other industries.

As startups took their Ozempic shots and slimmed down engineers and salespeople, it became clear that these companies would downshift to slower growth. Valuations descended by as much as 90% as the market reset expectations for everybody. They remain roughly as depressed today five years on from the bloodbath. As the Financial Times noted this week, software buyouts by PE firms hit a post-Covid low and don’t look set to recover any time soon.

Outside of the monopolies, American software companies are arguably more stable today than they were five years ago with their focus on profitability. But their ambitions have been neutered, sometimes to the point of merely attempting to survive without raising another round of capital. Operating margins crept up into positive territory for the first time in the industry’s modern existence, but at the direct expense of the future. That’s a retreat, and empires rarely survive on the back foot.

America’s own Brexit: the economic suicide of the techlash

America is globally dominant in software since the best people in the world come here to work on it. Intake is centered around universities, where the world’s brightest students come to learn the hardest subjects before entering industry and securing permanent residency and ultimately U.S. citizenship. It’s a system with plenty of faults, not least of which is the deeply circumscribed pathways for high-skilled immigrants allowed under existing laws.

Nevertheless, the system works. The key is not just the existence of pathways, but the legendary icons that exemplify just how successful taking those paths can be. Consider Sundar Pichai, who came from India to study at Stanford and Wharton, joining Google in 2004 and rising all the way to CEO. That’s a mirror of Satya Nadella, who did much the same in his rise to CEO of Microsoft, first coming to the United States to study at Wisconsin-Madison and Chicago before joining the Redmond giant in 1992.

It’s not a surprise their biographies read so similar: this is the immigrant pathway that works in America for high-talent individuals. It’s well-trodden, fully-explained by online guides and immigration attorneys, and it offers a well-understood reward at the end for those who work hard and follow the rules. Plus, by coming as still-impressionable students, they can absorb the best facets of America’s entrepreneurial culture.

Consistency is crucial. Immigrating to America is a decade-long affair from start to finish. Workers need to organize their entire lives — and roughly one quarter of their careers — to make it happen. Everyone wants to repair a system that is clearly creaking, but its best feature is the one least heralded: it simply doesn’t change. Immigration’s status as a cultural lightning rod for American politics has offered the ironic benefit of making it nearly invariant to the whims of different officeholders. Workers who organize their lives to “make it” in America will ultimately do so.

That stable continuity has become increasingly volatile. The executive branch has pulled immigration back from its stasis in Congress, with increasingly arbitrary changes and reversals. Citizens of whole countries are banned (now numbering 75), ranging from the understandable like Somalia to the befuddling like Thailand. H-1B lotteries start charging massive fees, then they’re reversed, then they are re-organized — all in the span of a few months.

A sudden lurch in policy three weeks ago required every H-1B employment visa holder to apply for U.S. permanent residency exclusively from abroad, with no clear guidance on whether they’d have to go now or later or when. Tens of thousands of H-1Bs adjust their status through this system every year by staying in America and waiting their turn. Days later, the policy was … reversed? Memory hole’d? It’s honestly like it never happened. But it could happen again, and every immigrant is watching with trepidation.

The best global talent has mobility, with America as the default by a wide margin. But as America starts to destroy the well-worn paths through the thickets of expatriate life, suddenly other paths look a bit more inviting. Is it better for an Indian engineer to move to Silicon Valley and work at OpenAI, or to try to move to Suwon and work at Samsung? That decision was incontrovertibly in America’s favor just two years ago, but now? It’s still the default, but it’s not a guarantee. It’s now a decision where an immigrant weighs the benefits and costs.

America’s entrepreneurial dynamism and software hegemony is heightened by the strength of the talent flowing into the industry. The zero-sum thinking that consumes the immigration debate more broadly was historically rejected in Silicon Valley, where it was obvious that new startups create positive-sum wealth. Growing insecurity among the professional classes though seems to be seeping into that consensus, to the point that I now regularly hear software engineers and even some founders demand a stop to H-1Bs. That’s ominous for the empire.

The immigration backlash dovetails with the wider American techlash, which is the worst I have seen in my lifetime and arguably in the country’s history. Labor unions certainly fought back against the depredations of the Industrial Revolution, but this was mostly over wages and working conditions rather than sheer hatred for material progress. In fact, anti-progress is one of those patterns that show up consistently in European history yet feels alien to America. The whole point of the country is to make technological, political and social leaps into the future — that’s why its founders left, after all.

Now, growing economic and social insecurities have found their target, and it’s the warrens of servers and networking cables in the concrete box down the street. The aggressive progressivism of American history is only coupled by the country’s retrograde impulse to stop change near us. NIMBYism rears its ugly head, first for housing and now for tech’s cathedrals of compute. Notably, America’s software empire could easily survive a slowdown in the data center buildout. It could build overseas, or it could make AI models more efficient and use the compute already on hand. This is an optimization problem that can be engineered.

What’s more alarming is that the techlash is expanding its scope. State governments are implementing ID laws to regulate the web, from controversial platforms like OnlyFans and prediction markets like Kalshi and Polymarket to the information sources that Americans consume. Privacy legislation is coming for the surveillance capitalism that underpins the monopoly engines of Alphabet and Meta. Schools and state governments are banning young people under 16 from using smartphones and social media. Meanwhile, state governments want the same technical interoperability that their European cousins are clamoring for and which I’ll talk about more shortly.

Many Americans see these policies as reasonable after decades of tech expansion. But that’s precisely the point: criticism of the empire is now passing through city councils and legislatures, and that’s after prodigious funding from industry on lobbying and community benefits.

Perhaps most ominously, there is intensifying anger toward venture capital as a business model. Tech is increasingly the only dynamism in the American economy, so we are what gets regulated and taxed. That’s led OpenAI to open conversations about offering equity to the U.S. government as a way to placate the angry mob.

Flinging shares to the government won’t salve the techlash though. Making Americans nominal co-owners won’t suddenly make them think twice about destroying these companies. The vitriolic hatred is too much for that, and both parties can see the advantages of coming down hard on the tech industry.

That populist anger is continuing to add fuel to the antitrust fire that threatens to burn down software. The Lina Khan-ites remain just as hardened about this direction, and no doubt see the growing techlash as their opportune moment to strike. Targets include Arm, the chip architecture that powers much of the mobile economy which was just targeted in a new probe, as well as potentially Microsoft again.

Unfortunately, a series of domestic blows to America’s software empire right as the world is transitioning into the intelligence age couldn’t come at a worse time. It truly is a Brexit moment for the country, in which a major wrong decision could create a generational loss of wealth and economic prosperity. Slowing international talent, stopping data centers, regulating apps and platforms, and breaking up the country’s strongest-performing companies have the combined potential to dismantle this invincible empire.

Global governments want to lockout American software lock-in

I’ve been emphasizing American software companies not out of parochialism but raw data: Europe’s inability to build a single globally powerful software company is legendary. The Old Continent has seemed to sustain its legacy almost intentionally, preferring to be the world’s museum rather than its experimental laboratory. Salaries are low, vitality is etiolated, and ambition has been absent.

Outside of a few anti-American intellectuels in France, no one cared what search engine Europeans used. Of the Mag 7, only Amazon has really struggled in Europe with its retail segment, fighting with everyone from labor unions to shopkeepers to build its distribution centers and implement its ecommerce methodology. Otherwise, Apple devices are aplenty, Windows runs across government laptops, and Google services are ubiquitous. Even Alphabet and Meta’s ad networks survived the onslaught of GDPR.

That coziness with American software power has changed in the last decade, gradually and then all at once. The gradual shift came in the form of European Commissioner for Competition Margrethe Vestager, who led an expanding group of policymakers, lawyers and civil society types to regulate and break up American big tech companies and their profitable monopolies. A myriad of explanations were given for why she was doing her work, but the most important is also the simplest: in Europe, big is bad. Her campaign partially succeeded, extracting large penalties from Alphabet as well as Apple and Meta. Much of the litigation around this is on-going.

Then Trump returned. Arrayed behind him at his inauguration were the chieftains of tech, and he offered them a solution. He would stop Europe’s attacks, but with a catch: they would become new arms for direct American influence in Europe. Our tech companies wouldn’t quietly lobby in Brussels to secure advantageous policies, but would aggressively seek to mold Europe’s software economy into America’s image.

Suddenly, the gauloise-smoking, Burgundy-drinking, anti-American French intellectuel complaining about European vassalage had a point. Politicians first perked up, and now they are starting to take action.

That starts with EU President Ursula von der Leyen. Through new legislation she is sheepherding, her goal is to broadly eliminate American software platforms from Europe, particularly in cloud and government services. According to the Centre on Regulation in Europe, roughly 80% of Europe’s “digital products, services, infrastructures, and intellectual property” rely on foreign providers. The EU wants to fund homegrown companies that take advantage of open-source products so that Europe can run on sovereign infrastructure.

This is much less of a lift than it might at first appear. Software lock-in has been weakened by mandatory interchange formats and better procurement. Eliminating these products and terminating their contracts is a project that can take place in a matter of a few months, not years. Cloud infrastructure is generally more embedded in workflows, but even here, better architectures often mean that individual components can be rewritten in sequence. Ironically, American products like Cognition’s Devin, Claude Code and other tools could accelerate this transition.

European governments are taking other actions, such as the Netherlands blocking the American takeover of Solvinity which powers the country’s digital ID systems and the United Kingdom dumping Stripe for Adyen. Expect more actions like this to come.

Europe has always been friendlier to American tech companies than many other countries. China is hermetically sealed with its Great Firewall, but even countries like Korea, India and Brazil have long protected their domestic software industries, often deadening innovation in the process. Europe’s past friendly social contract now increasingly looks like an abusive relationship and one that intends to sever.

This new movement for sovereignty dovetails with the growing excitement around open-source AI models. The incredible breadth and diversity of AI models and their developers doesn’t seem to be a ZIRP-like bubble phenomenon, but a sustainable and long-term pattern that will fundamentally cut the monopolization power of a handful of frontier models.

Why? Fred Brooks in his famous book The Mythical Man-Month once described what he dubbed the second-system effect. When building a new piece of software, engineers make terrible design decisions. They will over-engineer one part of the system that doesn’t matter while they overlook a critical feature that later proves to be the most valuable. The argument is that once a system is built, it’s a kludge, but a “second system” will be much better since all of the knowledge from the first system can now be used from the beginning.

I often reuse his model well outside of software engineering. Japan piloted a model of economic development helmed by its bureaucrats, but it later found itself lost in the 1990s after the boom years. When Korea was going through the same process, I was asked by many in the early 2010s when it would similarly reach its lost years. My response was always, “But the Koreans see what happened to Japan, and they know they have to avoid that outcome.” The fast follower has a unique advantage if the market leader stumbles or is just stuck with their initial forays into a new category.

OpenAI, Anthropic and Google DeepMind are the global leaders in the intelligence age. But countries have learned from their past lackadaisical strategies to harness mobile, cloud and social. Industrial policy now isn’t decades behind, but rather, nations as disparate as the United Arab Emirates, Saudi Arabia, Israel, Korea, China, Taiwan, France, the Netherlands, Switzerland and others have invested to stay as close to the frontiers across the stack, from energy and compute to data and models. Yesteryear’s submissive acquiescence has now become an intensifying rebellion against America’s dominance.

Most countries don’t have frontier labs, so their industrial policies tend to center on open-source AI models. As I noted before, software lock-in is not what it used to be. Purchasers are much smarter about how proprietary formats and protocols lock them into closed ecosystems and make them horrifically dependent on monopolistic and predatory providers (second-system effect!)

AI’s architecture is being built from the ground up for that networked and redundant world. Companies, mostly Chinese, are offering high-performance (if not bleeding-edge) models for free on the internet that anyone can run on their own infrastructure. OpenAI’s GPT 5.5 and Claude Fable 5 are absolutely better, but with tradeoffs in mind, most customers want to own their software and perhaps have a slight performance hit rather than use the best-of-breed option and be permanently reliant on an unstable partner.

Case in point: Anthropic’s launch this week of Fable 5 also mandates that the company can retain all queries and data, even for secure enterprise customers. Then there’s the company’s Mythos model. The Financial Times reported that Anthropic offered it to the National Security Agency for offensive cybersecurity operations before it offered the model to the rest of the American government, let alone America’s key allies. Thinkers in Paris, London, Seoul, Beijing, Tokyo and New Delhi can read, you know? To be reliant on American models means to be always at America’s mercurial mercy.

The openness here doesn’t mean that Europe or Asia are suddenly going to garner their own monopolies at the expense of America’s software empire. Instead, their strategy is to undermine the very profits that come from monopolies in the first place by injecting more competition in the market to crush American margins. It’s a strategy that won’t be easy, but has more force behind it than ever before.

The empire will strike gold, if not back

America’s software empire is at its pinnacle. The growth, the scale, the power — it’s almost unfathomable. It can be hard to see the cracks in such a strong facade, but they are there if we look for them carefully. America can neuter the techlash, of course. Unfortunately, it can do far less about the declining value of software given changing technology nor the broader movement of governments seeking economic security through sovereignty.

For software companies, global aspirations may dim even if they take a larger share of the domestic economy. Google may make more revenue even as Docs increasingly fades in other corners of the globe. Microsoft can always place more of a grip on American enterprise and Pentagon spending even as the defenestration of Windows in the data center continues abroad.

Yet, shrinking global aspirations have a tendency to cause a feeling of decline regardless of how margins adjust. America’s top software companies have boundless ambitions. They don’t just want to make an impact, they want every person in the world to use their products. Maybe SpaceX will judo other governments through space-based data centers and avoid such pesky things like national regulations. I doubt it. Even a small shrinkage of American ambition is something that will be hard to counteract.

That’s tough for the software industry, but it portends at least some renewal for the American venture capital industry. Even as 40% of VC investment heads to just ten companies in the United States, it’s clear that VCs are increasingly looking overseas for new companies, often precisely because of the new market opportunities that sovereignty affords. Breaking up markets offers more potential targets for returns, avoiding the acquihire-and-license AI system that has dampened some domestic VC profits. Countries may be sensitive to some sources of capital, but they must balance having a competitor that’s funded with foreign capital or just not having a player at all. More countries are becoming pragmatic.

American software had one of the greatest runs in business. If it carefully manages expectations, it will not become a fable of hubris and loss, but a Fable at the nexus of the global economy.

No AI was used in the production of this essay. Haters of my love of the em dash can have their Claude agents send me an angry mail.

Also check out

PRC-linked influence operations are targeting AI debates in the United States.

Germany is spending 100 billion euros to make its trains run on time. Will it work?

Chinese AI might not be an obvious first choice here. But it is in many parts of Africa.

Mr. Beast hits 500 million, but what’s it all for?

This is the deeper meaning of AGI Supremacy. The United States may try to preserve global AI dominance by treating frontier models as national-security assets. But the more openly Washington exercises this control, the more developers, companies, and governments will look for alternatives. American control may create short-term advantage, but it will also accelerate the global search for sovereign AI.

The Anthropic shutdown shows the basic template. When AI becomes powerful enough, it can be pulled into the national-security state. Today, the target is Fable 5 and Mythos 5. Tomorrow, it could be a model that accelerates cyber operations, weapons research, scientific discovery, industrial design, or strategic planning. If AGI arrives inside this framework, it will not be released as a neutral global commons. It will become a controlled strategic asset. In the age of AGI Supremacy, the final line of defense is local control: run an Opus-level model on your own GPUs, and no company or government can take it away from you.